Below is the performance between week 8 and week 12 against the benchmark:

Returns for this period were quite negative, but as remarked in an earlier post negative absolute returns are not necessarily a sign of poor portfolio management - returns need to be considered relative to a benchmark. In this case the benchmark has performed considerably worse. The client's portfolio lost 1.71% whereas the benchmark index has fallen almost twice as much, by 3.34%.

As noted in the previous post, adjustments made to the portfolio in week 8 did tend to reduce the duration of the holdings. Thus, perhaps the client's portfolio has mitigated losses in this period more effectively than the benchmark. Let's move on to consider the full sample of 12 weeks so that the data collected so far can be combined and analyzed in a more statistically significant manner.

Below is a the graph of performance over the full 12 weeks against the benchmark:

Surprisingly the constructed portfolio has outperformed the benchmark considerably. Looking at the full picture, this may due to the biggest price shifts occurring in the last 4 week period.

Overall, the client's portfolio returned 1.93% in 12 weeks. In comparison, the benchmark index returned only 0.33% due to poor performance in the last period.

Before assuming that this is enough to signify out-performance and claims of superior effective management, let's look first at how the performance is attributed in Bloomberg.

The attribution analysis shows that of the 1.60% excess returns compared to the benchmark, 0.78% was due to foreign exchange rate differentials, 0.66% was due to superior selection among individual assets, and 0.14% was due to improved allocation among sectors.

The performance by attribution shows a more measured level of success in the management of the portfolio. One figure that is particularly pleasing is the 0.66% of active returns due to selection. This holds considerable significance because it was also the selection figure that showed superior returns in the 1 year backdating test (which showed +3.16% due to selection). I believe this shows a firm indication that the general diversification strategies employed have been effective.

Let's continue on the the statistical summary over the 83 days of portfolio management:

These figures estimate the annualized mean return for the client's portfolio at 12.84%. This is certainly an impressive figure for a 100% fixed income portfolio tailored towards a low-medium risk profile.

Furthermore, the primary indicators for portfolio volatility show that the constructed portfolio was more consistent than the benchmark. The correlation measure has decreased compared to the backdated value of 0.89, this perhaps indicates some departure in strategy due to the implemented active management week 8 changes.

Overall, the evidence certainly suggests that the client's portfolio has been effectively diversified to achieve a returns comparable to those of a much larger index fund. In addition, a significant portion of the excess returns have been consistently attributed to the selection of stocks by the fund manager. Finally, the active management strategies implemented in week 8 showed promising results for further gains to be made if the client chooses to retain the portfolio management services provided over the past 12 weeks.

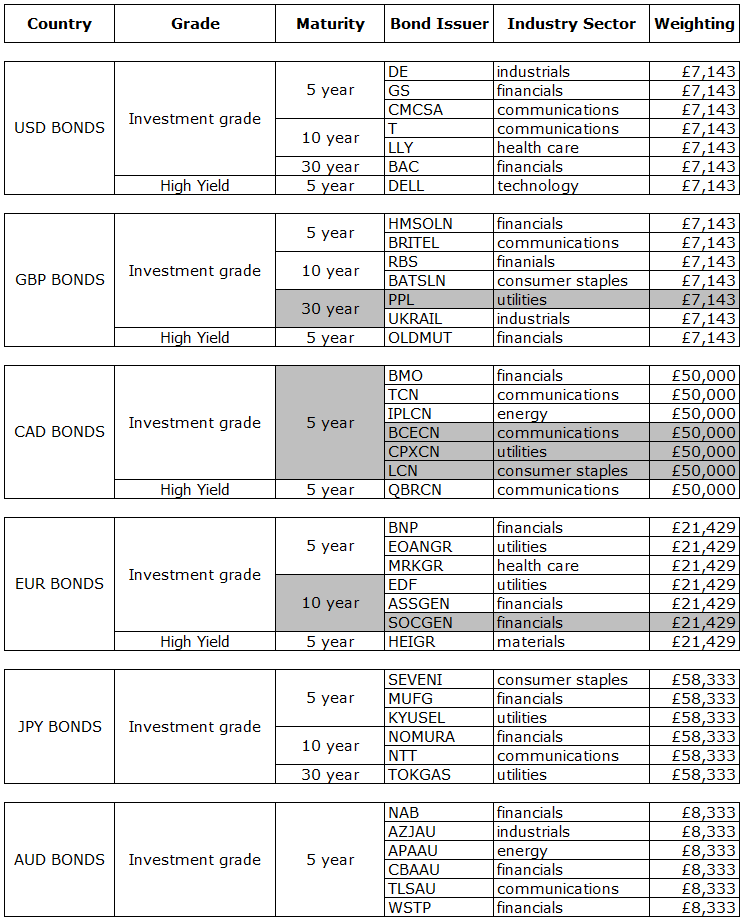

Provided below is the final composition of the portfolio in detail:

--

{kind=link}